Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

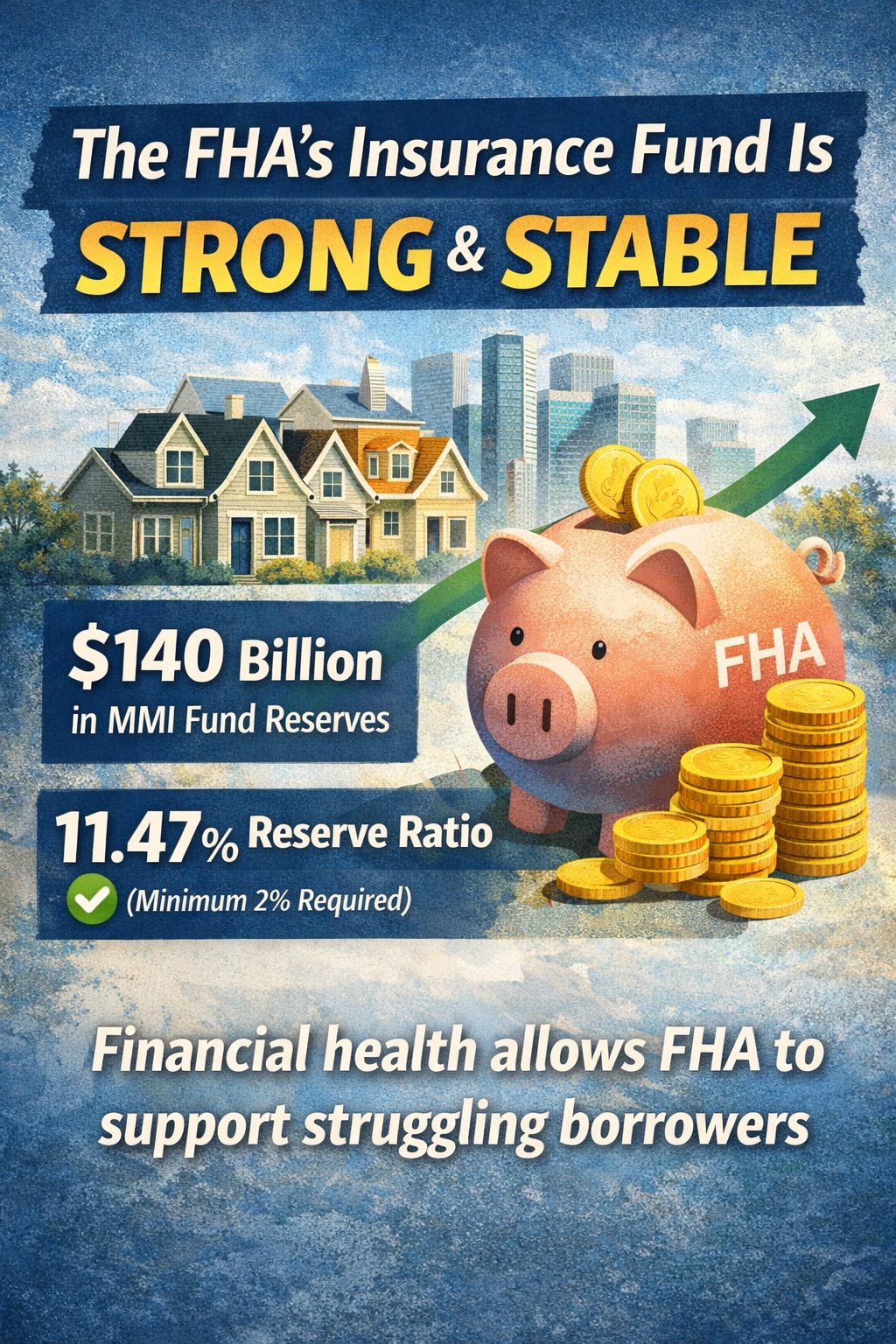

The FHA’s Insurance Fund Is Stronger Than Many Think

The Federal Housing Administration plays a major role in the housing market. It insures mortgages made to buyers who often have lower down payments. To protect lenders, the FHA uses an insurance pool called the Mutual Mortgage Insurance (MMI) Fund. This fund collects mortgage insurance premiums from borrowers. It then pays lenders if a borrower defaults. By law, the fund must keep reserves equal to at least 2% of its insured loans. Today, that reserve is far higher. According to recent data, the MMI Fund holds roughly $140 billion. Its capital reserve ratio sits at 11.47%. That level is well above the required minimum. It also signals strong financial health.

Why a Strong FHA Fund Matters

A well-funded insurance pool gives the FHA flexibility. It allows the agency to support borrowers during financial stress. At the same time, it helps stabilize the broader housing market. When the fund is weak, policymakers worry about rising defaults. When it is strong, the FHA can act without creating panic. This strength reduces the risk of sudden foreclosure waves. It also lowers the chance of forced home sales flooding local markets. For investors and housing professionals, that stability matters.

How FHA Borrower Relief Works Today

The FHA offers several loss mitigation tools. These include loan modifications, partial claims, and temporary payment relief. The goal is to help borrowers recover while protecting the insurance fund. However, repeated assistance caused problems in the past. Many borrowers redefaulted within a short time. Because of this, the FHA updated its rules in 2025. Borrowers now face limits on how often they can receive help. They must also show they can resume payments. These changes aim to reach faster and clearer outcomes.

What This Means for the Housing Market

For real estate professionals, the takeaway is simple. The FHA is not fragile. Its insurance fund is strong and well-managed. This reduces uncertainty around FHA-backed inventory. Homes are less likely to sit in long distress cycles. Instead, outcomes may become more predictable. Overall, the FHA’s financial position supports market stability. It also provides important context for buyers, sellers, and investors watching future housing supply.